All Categories

Featured

Table of Contents

The technique has its own benefits, but it additionally has issues with high costs, complexity, and a lot more, resulting in it being considered as a rip-off by some. Unlimited financial is not the most effective policy if you need just the investment element. The limitless banking idea rotates around making use of whole life insurance policy plans as a monetary device.

A PUAR allows you to "overfund" your insurance plan right approximately line of it ending up being a Changed Endowment Agreement (MEC). When you utilize a PUAR, you quickly increase your cash money worth (and your death benefit), therefore enhancing the power of your "bank". Additionally, the more money value you have, the greater your passion and dividend repayments from your insurance policy firm will certainly be.

With the surge of TikTok as an information-sharing platform, financial recommendations and methods have found a novel way of dispersing. One such strategy that has actually been making the rounds is the infinite banking principle, or IBC for short, garnering recommendations from stars like rap artist Waka Flocka Fire - Infinite Banking. Nevertheless, while the technique is currently preferred, its origins map back to the 1980s when financial expert Nelson Nash introduced it to the world.

How long does it take to see returns from Infinite Banking Retirement Strategy?

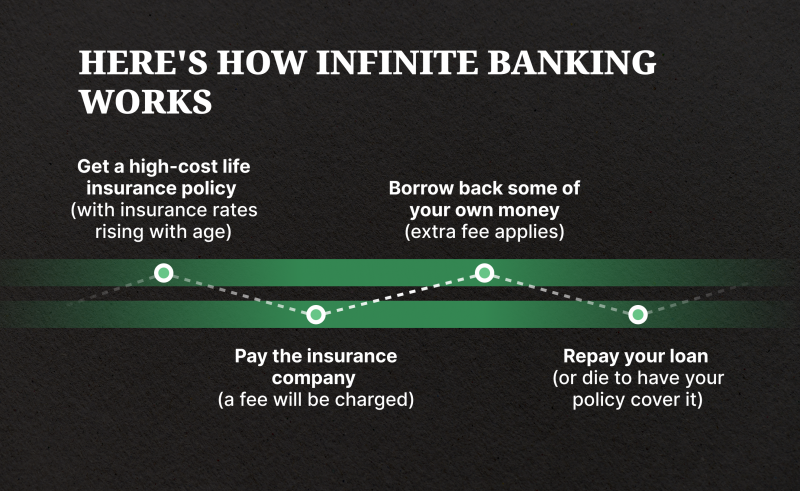

Within these plans, the cash worth grows based on a price established by the insurance firm. Once a considerable cash money worth builds up, insurance policy holders can get a cash money worth loan. These car loans differ from traditional ones, with life insurance policy offering as security, suggesting one could shed their insurance coverage if loaning excessively without appropriate money value to sustain the insurance coverage costs.

And while the appeal of these plans appears, there are natural restrictions and threats, requiring thorough cash worth tracking. The strategy's legitimacy isn't black and white. For high-net-worth individuals or company owner, specifically those utilizing approaches like company-owned life insurance (COLI), the advantages of tax obligation breaks and compound development could be appealing.

The attraction of unlimited banking doesn't negate its challenges: Cost: The foundational need, an irreversible life insurance coverage plan, is more expensive than its term counterparts. Qualification: Not every person gets whole life insurance policy due to rigorous underwriting procedures that can omit those with details wellness or way of living problems. Intricacy and threat: The complex nature of IBC, paired with its dangers, may prevent numerous, particularly when simpler and much less dangerous choices are readily available.

Policy Loans

Designating around 10% of your regular monthly revenue to the policy is simply not possible for the majority of people. Using life insurance policy as a financial investment and liquidity source requires technique and tracking of policy cash value. Seek advice from a monetary consultant to determine if limitless financial aligns with your concerns. Part of what you read below is just a reiteration of what has currently been said over.

Prior to you obtain on your own into a scenario you're not prepared for, recognize the following first: Although the idea is frequently sold as such, you're not really taking a loan from on your own. If that were the instance, you would not have to repay it. Rather, you're obtaining from the insurance provider and need to repay it with rate of interest.

Some social media articles suggest making use of cash worth from entire life insurance policy to pay down credit history card debt. When you pay back the financing, a part of that interest goes to the insurance policy firm.

How do interest rates affect Generational Wealth With Infinite Banking?

For the very first numerous years, you'll be repaying the payment. This makes it extremely hard for your policy to collect worth throughout this time. Entire life insurance policy prices 5 to 15 times much more than term insurance policy. Many people simply can't manage it. So, unless you can pay for to pay a couple of to a number of hundred dollars for the next decade or more, IBC will not benefit you.

If you require life insurance, below are some valuable ideas to consider: Consider term life insurance coverage. Make certain to go shopping about for the ideal price.

What type of insurance policies work best with Privatized Banking System?

Visualize never needing to stress regarding bank financings or high rate of interest rates once more. What if you could obtain money on your terms and build wealth all at once? That's the power of infinite financial life insurance. By leveraging the cash value of entire life insurance policy IUL policies, you can expand your wealth and borrow cash without relying upon typical financial institutions.

There's no collection lending term, and you have the liberty to make a decision on the payment routine, which can be as leisurely as repaying the loan at the time of fatality. This flexibility reaches the maintenance of the finances, where you can opt for interest-only repayments, keeping the financing balance flat and convenient.

Can I use Borrowing Against Cash Value to fund large purchases?

Holding cash in an IUL repaired account being attributed rate of interest can frequently be much better than holding the money on deposit at a bank.: You have actually always fantasized of opening your very own bakeshop. You can obtain from your IUL plan to cover the initial costs of leasing a room, purchasing tools, and hiring team.

Individual financings can be obtained from standard financial institutions and debt unions. Borrowing cash on a credit scores card is normally really costly with yearly portion rates of interest (APR) frequently reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Nelson Nash Bank On Yourself

Infinite Banking Solution

R Nelson Nash Net Worth